Got a busted toilet in your place in Japan? Check for this before you pay the whole repair bill.

When moving into a new apartment in Japan, there are a lot of different payments you have to make. There’s the first and last month’s rent, security deposit, real estate agency fee, the one-time move-in fee paid to the landlord called “key money,” and the fee for actually changing the locks and making new keys. So by the time you get to the part of the process where you’re required to pay for “fire disaster insurance,” you’ll probably just shrug your shoulders and say “Yeah, that makes sense” without reading all of the fine print.

But here’s the thing about “fire disaster insurance”: it doesn’t just cover you against fire damage, and sometimes it also works as toilet insurance.

First, let’s take a quick look at the linguistics for this required insurance for renters. In Japanese it’s called kasai hoken, which is written in kanji like this.

This does literally translate as “fire disaster insurance.” The first kanji, 火, means “fire,” and the second 災, is “disaster.” Together they become 火災, kasai, meaning a destructive fire (as opposed to, say, a cooking fire or campfire). And 保険/hoken is the Japanese word for “insurance.”

But even though the name only mentions fire, kasai hoken is really an umbrella policy that covers all sorts of unpleasant situations. In addition to fire, it also usually functions as insurance against flood, wind, snow, hail, and water damage, and sometimes even certain instances of damage as a result of flying object impact and theft. And as we mentioned above, your “fire disaster insurance” may also cover damage to bathroom fixtures like your bathtub, washbasin, and toilet.

We found this out recently when one of our Japanese-language reporters, Ahiruneko, was moving out of his old apartment, which got him thinking about his recently broken toilet seat.

Since the bowl itself is OK, Ahiruneko had just kept on using the toilet without getting the seat fixed. As part of the process of moving out, though, the landlord would be doing a final check of the apartment, and Ahiruneko figured the cost of the toilet repairs was going to come out of his deposit. What’s worse, since it’s a fancy washlet-style toilet, he figured it wasn’t going to be cheap to fix.

So he asked his landlord whether repair costs for the toilet might be covered under his kasai hoken policy. The landlord told him he’d have to check with the insurance provider, so that was the next call Ahiruneko made, and to his happy surprise, they told him that yep, his “fire disaster insurance” also works as toilet insurance.

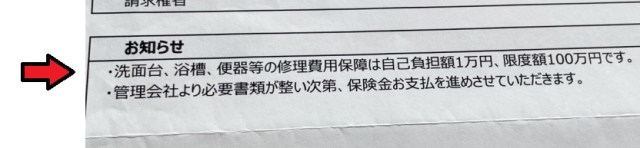

The section of Ahiruneko’s insurance contract that the arrow is pointing to in the above photo indicates that repair costs of up to one million yen (US$6,850) for his apartment’s toilet, washbasin, or bathtub are covered, with Ahiruneko having to pay just 10,000 yen out of his own pocket. This turned out to be great news, because when the landlord came by for his pre-move-out inspection, they assessed that it was going to cost 28,000 yen to repair the toilet.

So in the end, Ahiruneko’s “fire disaster insurance” ended up saving him 18,000 yen in toilet repairs, more than half the total bill.

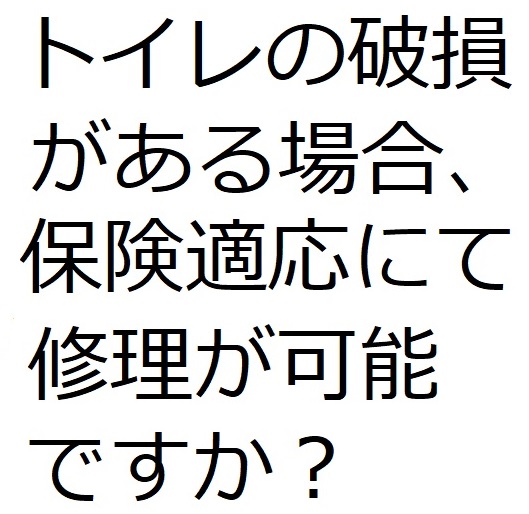

We should note that the exact details of kasai hoken coverage may vary by insurance provider. If you want to check if yours will cover toilet repairs, you can ask the customer service rep “Toire no hason ga aru baai, hoken tekiou nite shuuri ga kanou desu ka?”, which means “In the case of damage to the toilet, can my insurance be applied to the repairs?”

▼ That same phrase, written in Japanese

If you want to change that to asking about the bathtub, all you have to do is swap out toire (トイレ) and put in yokusou (浴槽), and if you’re asking about the washbasin, the word to use is senmendai (洗面台).

If the fixture that needs fixing is covered by your insurance, the exact process for filing the claim also may vary by provider, but in general you’ll need a document confirming the repair cost from your landlord, which will then need to be supplied to your insurance provider. In Ahiruneko’s case, he ended up having the full repair cost of 28,000 yen deducted from his security deposit, and after that he received a notice from his insurance provider saying that they had approved his claim and sent the money to his landlord, who then transferred the money into his bank account. With all that sorted out, though, he’s got 18,000 extra yen in his pocket, and he’s thankful that his “fire disaster insurance” kept him from getting burned for the full repair bill.

Reference: General Insurance Association of Japan

Images ©SoraNews24

● Want to hear about SoraNews24’s latest articles as soon as they’re published? Follow us on Facebook and Twitter!

[ Read in Japanese ]

What to do if you want to lower your apartment rent or avoid paying key money in Japan

What to do if you want to lower your apartment rent or avoid paying key money in Japan Here’s one of the first things you should do if you just moved into a new apartment in Japan

Here’s one of the first things you should do if you just moved into a new apartment in Japan Japan has a cat real estate agency, where every apartment lets you and your kitty live together!

Japan has a cat real estate agency, where every apartment lets you and your kitty live together! The pros and cons of living in a share house in Tokyo instead of an apartment

The pros and cons of living in a share house in Tokyo instead of an apartment How much money do you need to live in your own apartment in Japan?【Survey】

How much money do you need to live in your own apartment in Japan?【Survey】 Studio Ghibli releases the My Neighbour Totoro tea caddy, with a magical self-closing lid

Studio Ghibli releases the My Neighbour Totoro tea caddy, with a magical self-closing lid 7-Eleven Japan releases a crazy new viral sandwich: Chocolate Sprinkles and Whipped Cream

7-Eleven Japan releases a crazy new viral sandwich: Chocolate Sprinkles and Whipped Cream Public restrooms in Osaka to get in-stall video screens with ads

Public restrooms in Osaka to get in-stall video screens with ads New cherry blossom party picnic essential: This super-handy folding cardboard table

New cherry blossom party picnic essential: This super-handy folding cardboard table Japanese department store rooftop is a secret oasis where you can escape the crowds in Tokyo

Japanese department store rooftop is a secret oasis where you can escape the crowds in Tokyo Starbucks Japan releases first-ever Hinamatsuri Girls’ Day Frappuccino

Starbucks Japan releases first-ever Hinamatsuri Girls’ Day Frappuccino Japan now has a “for foreign tourists only” Mt. Fuji sightseeing train[Video]

Japan now has a “for foreign tourists only” Mt. Fuji sightseeing train[Video] Japanese man drives truck that’s on fire directly to fire station, drops flaming potatoes[Videos]

Japanese man drives truck that’s on fire directly to fire station, drops flaming potatoes[Videos] Instant tempura and abura-age from Cup Noodle maker Nissin coming to power up your noodle meals

Instant tempura and abura-age from Cup Noodle maker Nissin coming to power up your noodle meals Very limited sale of glasses that can halt or reverse nearsightedness begin in Japan

Very limited sale of glasses that can halt or reverse nearsightedness begin in Japan Starbucks Japan releases new My Fruit³ Frappuccino at only 34 stores around the country

Starbucks Japan releases new My Fruit³ Frappuccino at only 34 stores around the country Japanese onsen egg maker from 100-yen store Daiso needs to be on your shopping list

Japanese onsen egg maker from 100-yen store Daiso needs to be on your shopping list Cherry blossoms begin blooming in Japan with record-early starts for sakura season

Cherry blossoms begin blooming in Japan with record-early starts for sakura season Tokyo government organizes food truck event to clear out delinquent/homeless teen gathering area

Tokyo government organizes food truck event to clear out delinquent/homeless teen gathering area Nine amazing off-the-beaten-path cherry blossom spots in Japan for yaezakura and shidarezakura

Nine amazing off-the-beaten-path cherry blossom spots in Japan for yaezakura and shidarezakura Stunning central Japan wisteria festival is like a purple fantasy straight out of a Ghibli movie

Stunning central Japan wisteria festival is like a purple fantasy straight out of a Ghibli movie When will the cherry blossoms reach full bloom in Japan this year?[Forecast]

When will the cherry blossoms reach full bloom in Japan this year?[Forecast] Studio Ghibli unveils new Rollbahn notebook in honour of Howl’s Moving Castle

Studio Ghibli unveils new Rollbahn notebook in honour of Howl’s Moving Castle Studio Ghibli adds new anime tumblers to its cool streetwear brand in Japan

Studio Ghibli adds new anime tumblers to its cool streetwear brand in Japan Universal Studios’ Sailor Moon theme park attraction is finally coming to America

Universal Studios’ Sailor Moon theme park attraction is finally coming to America Starbucks Japan unveils new sakura cherry blossom collection for hanami season 2026

Starbucks Japan unveils new sakura cherry blossom collection for hanami season 2026 Train station platform ramen store closes its doors on half a century of history in Tokyo

Train station platform ramen store closes its doors on half a century of history in Tokyo Studio Ghibli releases Catbus pullback keychain that runs like the anime character

Studio Ghibli releases Catbus pullback keychain that runs like the anime character Nine great places to see spring flowers in Japan, as chosen by travelers (with almost no sakura)

Nine great places to see spring flowers in Japan, as chosen by travelers (with almost no sakura) Studio Ghibli adds new Mother’s Day gift sets to its anime collection in Japan

Studio Ghibli adds new Mother’s Day gift sets to its anime collection in Japan Virtual idol Hatsune Miku redesigned with look that adds new elements and brings back old ones

Virtual idol Hatsune Miku redesigned with look that adds new elements and brings back old ones Survey asks foreign tourists what bothered them in Japan, more than half gave same answer

Survey asks foreign tourists what bothered them in Japan, more than half gave same answer Japan’s human washing machines will go on sale to general public, demos to be held in Tokyo

Japan’s human washing machines will go on sale to general public, demos to be held in Tokyo Starbucks Japan releases new drinkware and goods for Valentine’s Day

Starbucks Japan releases new drinkware and goods for Valentine’s Day We deeply regret going into this tunnel on our walk in the mountains of Japan

We deeply regret going into this tunnel on our walk in the mountains of Japan Studio Ghibli releases Kodama forest spirits from Princess Mononoke to light up your home

Studio Ghibli releases Kodama forest spirits from Princess Mononoke to light up your home Starbucks Japan releases new sakura goods and drinkware for cherry blossom season 2026

Starbucks Japan releases new sakura goods and drinkware for cherry blossom season 2026 Japan’s newest Shinkansen has no seats…or passengers [Video]

Japan’s newest Shinkansen has no seats…or passengers [Video] Major Japanese hotel chain says reservations via overseas booking sites may not be valid

Major Japanese hotel chain says reservations via overseas booking sites may not be valid Put sesame oil in your coffee? Japanese maker says it’s the best way to start your day【Taste test】

Put sesame oil in your coffee? Japanese maker says it’s the best way to start your day【Taste test】 No more using real katana for tourism activities, Japan’s National Police Agency says

No more using real katana for tourism activities, Japan’s National Police Agency says Japan apartment hunting – Can you find cheaper rent by avoiding the peak spring moving season?

Japan apartment hunting – Can you find cheaper rent by avoiding the peak spring moving season?